How About an Insurance Rate Cut?

The term “insurance rate cut” is nothing new in monetary policy. After being absent for 11 years, the current Fed Chair Jerome Powell himself reintroduced that idea in July 2019 (more like a proposal a month earlier by the then St Louis Fed President James Bullard) in a series of three rate cuts, before Covid-19 pandemic struck the following year crashing the rate to zero.

See Top 10 Lowest Home Loan Rates

Insurance rate cut is when the Fed sees scenarios that could lead to slower growth, higher unemployment, disinflation or even deflation, and decides to take some pre-emptive action. The Federal Reserve Bank of Dallas had published a very detailed paper on the concept of insurance rate cuts or hikes back in 2019.

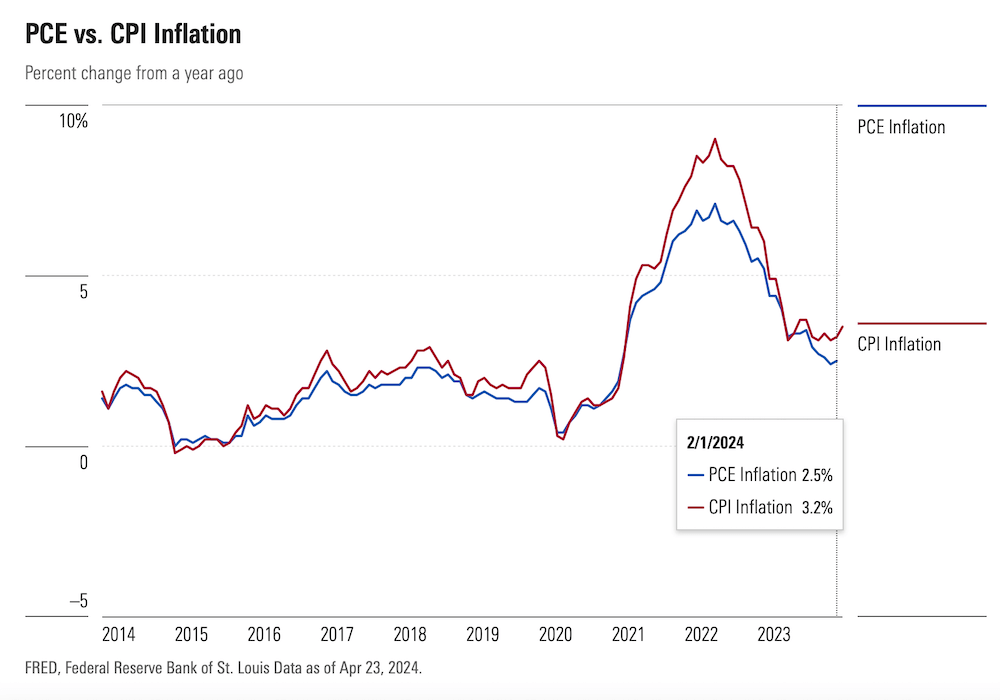

At the moment, the prospect of such a cut in July seems remote with the latest Fed minutes showing a voice of concern amongst many Fed officials that the progress on inflation has stalled. This was seen clearly from the chart below showing headline all-in (including food and energy prices) PCE and CPI. You may read this explainer on the difference between the Price Consumer Expenditure (PCE) and the Consumer Price Index (CPI) in the U.S.

Source: Morningstar.com

Inflation looks to be almost on a symmetrical path down from its peak of 9% at the start of 2022, until the downtrend stalls as we hit a slight uptick coming back into Q1 of 2024. This slight uptick has wreaked havoc on financial markets sending yields up since the start of the year. What you see above was the inflation print for the month of February; we have since logged new data which seems to affirm this uptick beyond just seasonality factors at the start of the year, with headline PCE and CPI reading at 2.7% and 3.5% for March respectively, both higher than in February. Market begin to brace for further increases following hot PPI (Producer Price Index) figures for April until suddenly headline CPI for April came in softer at 3.3% reversing the recent uptrend. Could this mark the return and continuation of the disinflationary forces that got disrupted somehow in Q1 of 2024?

See Top 10 Lowest Home Loan Rates

Whatever those factors causing inflation to be stickier in the last mile, Fed has opted to be patient so far. All eyes are now on the next PCE (Price Consumer Expenditure) reading, which is Fed’s preferred measure of inflation, that’s coming up on 31 May. In fact, the next few months’ CPI and PCE readings will carry significantly more weight than what the Fed has to say. The bond market is now pricing in the prospect of a first rate cut in September. From now till then, there are many data points that could change the whole narrative, especially if we start to see disinflationary pressures resuming, coupled with slower wage growth as well as a higher unemployment number breaking above the 4-handle (it was 3.9% in the latest reading for March)!

For one, I am not dismissing the possibility of Fed enacting an “insurance rate cut” as early as July, depending on all the data that’s coming out before the July FOMC scheduled on 30-31 July, which is still two months away. This time, the insurance cut will be to insure against Fed triggering an economic recession if they fail to act fast enough, as that’s how all monetary tightening cycles typically end in the past.

There’re a few more “academic” arguments for going earlier rather than later:

- Doing it way before the elections, instead of waiting for September, will get that political debate out of the way, albeit Fed is famously known to defend its apolitical stance.

- It’s almost exactly 12 months to the last hike on 26 July 2023. That’s also about how much time is needed for that long and variable lags of monetary policy to show up in the real economy. Typically, this could be 12-18 months which means you probably might expect the consumer to weaken and economy to slow more significantly in the second half of 2024.

- Fed has been criticised front and centre for being “behind the curve” and acting too slow in raising rates in 2021, allowing inflation to spike out of control; They certainly won’t want to make the same mistake a second time by acting too slowly and causing the economy to crash.

The feeling most Fed watchers have laid out this year is one where the Fed really wants to cut, and is dying to do so at the earliest given moment, provided inflation data cooperates enough to give them that excuse. Honestly, I see no wrong in the Fed simply stating matter-of-factly what an insurance cut is supposed to mean – acting early, but be prepared to pivot back and hike if necessary. It’s better to act early and reverse course than to act too late again.

Of course, I am no expect in monetary policy and I have no crystal ball as there’s a wide spectrum of possibilities from a first cut in July, to one in the much anticipated September, or perhaps none at all in 2024. But one thing is for sure, interest rates will have to come down either in 2024 or by 2025 one way or another. It’s either one or two pre-emptive insurance cuts by Fed, or worse, a whole series of reactive and sizeable cuts in event of a hard landing.

Fed has been criticised front and centre for being “behind the curve” and acting too slow in raising rates in 2021, allowing inflation to spike out of control; They certainly won’t want to make the same mistake a second time by acting too slowly and causing the economy to crash.

Like to compare home loan packages across all 10 major banks in Singapore?

At MortgageWise, we help clients navigate through the myriad of mortgage rates quick and fuss-free and get you the best home loan Singapore! Be it for residential or commercial property loan, work with us today and you’ll also be helping to support our social cause!

Stay tuned for rate alerts on our Telegram channel SG Mortgage Rates.

See Top 10 Lowest Home Loan Rates

Disclaimer: MortgageWise Pte Ltd is not in the business of providing financial advice nor are we licensed or regulated by MAS under the Financial Advisory Act (FAA) in Singapore. All information presented are opinions and any representations given, whether by way of example, illustration or otherwise, are purely portfolio allocation advice and not recommendations or inducements to buy, sell or hold any particular investment product or class of investment product. All opinions are generic in nature and are not tailored to the particular circumstances of any reader. Seek advice from a qualified financial advisor before making any investment decision.

Though every effort has been made to ensure the accuracy of the information and figures presented, we make no representations or warranties with respect to the accuracy or completeness of the contents in this blog and specifically disclaim any implied warranties or fitness for a particular purpose. We shall not be held responsible for any financial loss or any other damages suffered whatsoever, directly or indirectly, if you choose to follow any of the advice or recommendations given in this blog.