Local Banks’ Score Card 2018

As the three local banks have just reported their financial results for last quarter of 2018, let us take a look at the full year performance in 2018 for mortgages.

See Top 10 Lowest Home Loan Rates

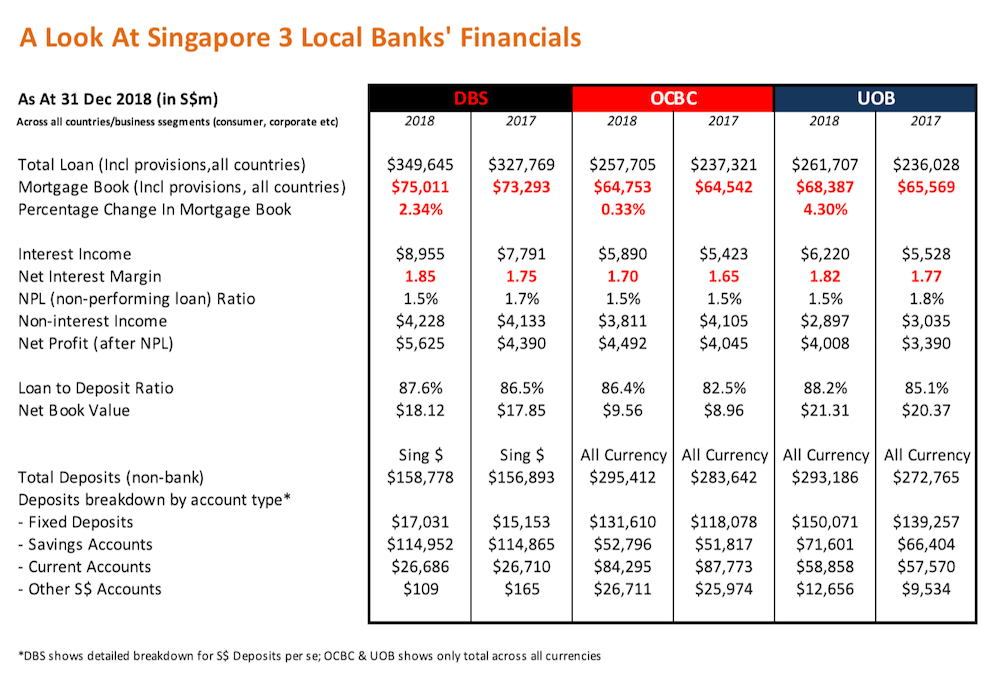

At the results briefing, it was reported DBS home loans still enjoys a commanding share of 31% of the mortgage market in Singapore. From MAS statistics on its website, we know the total mortgage market in Singapore as at end 2018 was at $207.5b based on total loans disbursed (exclude the insignificant bridging loans). This means (we can only estimate) that DBS share of outstanding loans is at $64.3b which is 86% of its total mortgage loan book across all countries.

In the absensce of breakdowns on mortgages in Singapore vs other countries, we can only draw conclusions in this article based on the entire mortgage books for all three banks (across all countries) and assumed that over 80% of their mortgage portfolio comes from loans in Singapore, like what we have seen in the case of DBS above.

Overall, UOB home loans exhibit the best performance in terms of loan books growth in 2018 whereas DBS grew the most in terms of NIM (net interest margin). The latter is hardly surprising as DBS has access to the largest pool of cheap Sing dollar funds in its millions of POSB CASA (current account savings account) accounts base that is out of reach of the other two banks. With 3-month SIBOR rising significantly in the year from 1.12% at end-January to end the year at a high of 1.89% in December, DBS sees exploding interest income from being the net lender (to other banks) in the interbank market. A look at its Sing dollar funds composite will reveal that CASA accounts contribute the lion’s share of 89% ($141.6b out of total $158.8b) of its source of funds. On the other hand, fixed deposits of mere $17b contributes only 11%. Remember the ubiquitous FHR (fixed deposit home rate) which is defined on smaller deposits of below $10,000 will account for even lesser of this $17b fixed deposit base. We assume this could be less than 20% (pareto’s rule), ie. $3.4b. This is why we have been saying any increases to FHR will hardly make a dent on the bank’s cost of funding.

On the contrary, fixed deposits form about half the source of funds for the other two local banks OCBC and UOB so the any increment to deposit rates would hit the bank’s bottom line a lot harder. That is also why both lenders have since discontinued pegging their home loans to FDRs (fixed deposit rate) but reverts back to offering home loans tied to BOARD rates since middle of 2018.

See Top 10 Lowest Home Loan Rates

In terms of loans book, OCBC home loans registered almost flat growth ending the year with the same $64b portfolio it started with. UOB grew its loans book the most at $68b, closing the gap on market leader DBS’s $75b slightly (gap of $7b down from previous year’s gap of $8b).

Interestingly this year, with sentiments on the ground shifting back towards SIBOR packages from what we have seen so far, lenders who do not offer competitive SIBOR packages might see further challenges in growing their portfolio. Foreign banks who have been nipping away market share from local banks of late with very aggressive pricing stand to make further inroads. Still we do not expect local banks to sit still and do nothing and the battle for market share will likely intensify from second quarter of the year onwards.

Homeowners who keep their ears to the ground will stand to benefit from this brewing mortgage war, and there’s no better way to do that than engage the service of a professional mortgage broker who can supply the latest promotional rates for refinancing, plus additional perks. At MortgageWise.sg, we offer the best comparison via our Rates Report that shows “whole of market” packages, and we bring you exciting cost savings like a $150 Valuation Fee Offset for refinancing and a $1,800 Legal Fee (inclusive of stamp duty & gst) for purchase, both subject to a minimum loan of $500,000. Get the best home loan Singapore by speaking to our consultants today!

Since 2014, MortgageWise.sg has provided thought leadership in the mortgage planning space in Singapore, taking deep dives into the latest developments in the industry, providing useful mortgage tips, and making sense of rate movements. We seek to build trust with clients over the longer term instead of doing product-peddling for quick one-time deals. That’s why we always present “whole-of-market” perspective including home loan packages that some banks do not pay us.

{kind=link}