Still Undecided – Fixed Or Floating Rate?

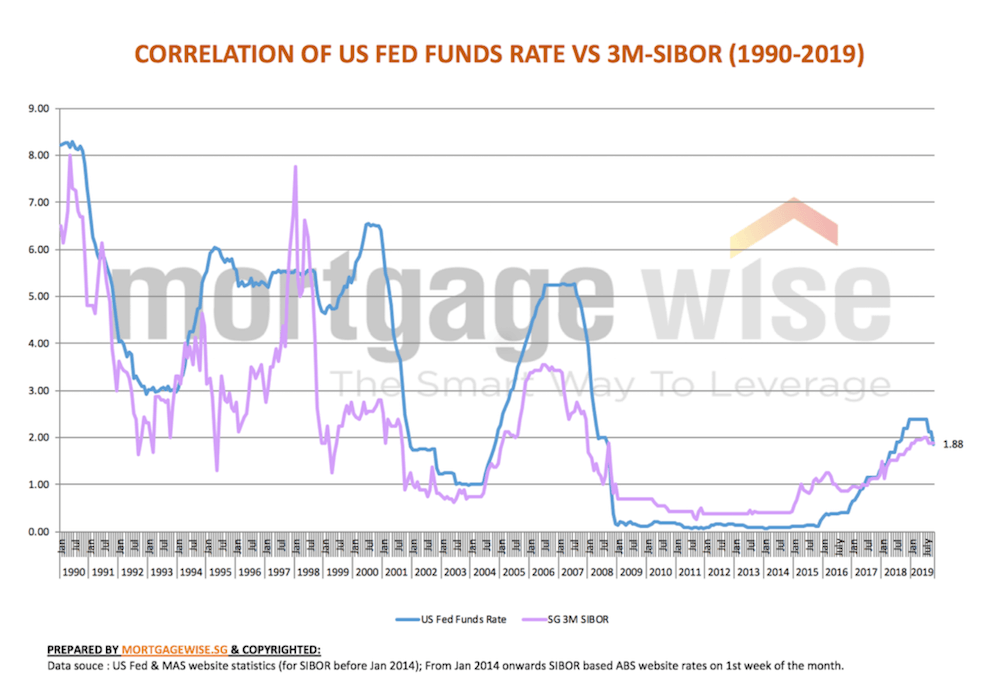

US Fed has cut rates twice this year in July and September, bringing the federal funds rate down by 50 basis point to below 2% now. All eyes are now on their next FOMC meeting at end of the month, October 29-30.

Still, SIBOR (Singapore Interbank Offer Rate) has stayed fiercely stubborn in the last four months as it refused to come off from 1.87-1.88% level since July. What has happened since is that we see 3-month SIBOR closed the gap with 1-month as it dropped from above 2% in June to be at parity with 1-month now with both at 1.87%. Traditionally there has always been a 10-15 basis points gap between the two (see our SIBOR chart).

Many are expecting SIBOR to drop at some point, especially if Fed cuts again and decline in global rates continue. While we cannot tell you precisely when SIBOR will eventually buckle, we can give you the historical perspective.

See Top 10 Lowest Home Loan Rates

Phase I Of Cycle

For many years before October 2014 (see graph below), nobody was interested in fixed rate home loans. That’s when oil prices crashed leading to a breakout of 3-month SIBOR (the benchmark interest in Singapore) from its low base of 0.40% for a long time. When interest rate started to rise more seriously from Dec 2015 (when Fed started its 1st historical rate hike, 9 in total), many opted for fixed rates from 1.38% to 2.20% only to see SIBOR tumbled back from 1.25% to 0.87% by the following year 2016. In fact, it was not until two years later in Feb 2018 last year that SIBOR got back from where it last left off at 1.25% to resume this accent. By this time, many homeowners who signed onto 2-year fixed rates from 2015 to 2017 did not quite benefit from paying the higher fixed rates. Prevailing floating rates during their lock-in period went back down to 1.30-1.40% level.

Phase II Of Cycle

The real steep climb in interest rates, as explained, really happened in recent times from Feb 2018 last year when 3-month SIBOR started to rise steadily from 1.25% to hit a high of 1.88% by end of 2018, and continued a futher rise to 2.0% before it peaked in July this year. That’s when US Fed started to cut rates for the first time in 3½ years. Again, this phase of rate increases lasted less than two years – just like the one before! Now if we take both phases (from 2015 to mid-2019) as one full interest rate up cycle when 3-month SIBOR first rose from 1.07% then dipped down to 0.87% before peaking at 2%, the cycle lasted less than four years. SIBOR has now retraced back to 1.87% and the big question is – are we in the middle of a mid-cycle pause before rates resume its up trend in 2020? Or are we past the peak and going into a cycle reversal downwards for the next few years, ie. an economic downturn or recession looming?

Homeowners refinancing in 2015-2017 may have concluded that those who opted for fixed rates always end up losing as the fear of rising interest never turn out quite as badly as what they perceive it to be – they would be better off taking a bet on floating rate home loans. There is some truth to that. Then come 2018, when banks started to take turns to hike mortgage loan pegs from FHR, FDR, FDPR, FDMR, OHR to BOARD rates. During this period, homeowners on floating rates would have seen their interest rates shot up on average a full percentage points to reach 2.2%-2.6% (our blog reports on all these rate increments). Repricing banks started fearmongering on rising rates at the start of this year and many would have signed onto fixed rates at 2.28%-2.48% in Jan-Mar 2019. Only to see a sudden US Fed reversal of stance in March, followed by a first rate cut by July. History is repeating itself.

See Top 10 Lowest Home Loan Rates

Why do we go through the events from 2015 until the first half of 2019? Well, it helps to frame the decision in the correct perspective even when we do not quite have the crystal ball anwser to that big question raised earlier – mid-cycle pause or cycle reversal in place?

Lessons From Recent Interest Rate Cycle

Two lessons we can conclude from past events on interest rates movements:

- Should interest rates buck the trend and start to rise again in the medium-term, it is not going to rise so quickly as to hit 3.5-4% in two years. And it is not certainly going to rise in a straight line, perhaps with some false starts along the way.

- Even if rates are going down further, it is already near the historical base level here in Singapore – which is floating rate at 1.20% and fixed rates at 1.38-1.48%. It may not even get to such low levels!

Hence, the risk of erring on the choice between fixed and floating has been reduced substantially. Put it in a more direct manner: Should one go for floating rate home loans with the view that SIBOR will drop off at some point, the usual lock-in period of two years is acceptable as rates are unlikely to spiral anytime in that short period. Should one go for a fixed rate home loans at the current 1.84-1.86%, it cannot be too wrong as we may or may not go all the way down to 1.48% for fixed rates before a sudden pickup. There is always that surprise element of a trade truce in 2020 with economic growth coming back after a long pause, albeit many are less optimistic of such a scenario.

Speak to our experienced team of mortgage consultants here who have been in the business long enough to witness the cycles and give caution where we see pitfalls ahead. Like how we were against going for fixed rates at the start of the year when it skyrocketed to 2.58%. It was inconceivable to us then, that rates would hit 3% or higher so quickly in the near term with so much uncertainties around. It makes better sense to opt for floating rates instead where one lets the average interest over a two-year lockin period rise up slowly, if at all. And on hindsight it hasn’t.

In this blog, we have provided you some basis to decide on fixed versus floating rate. First, we give you a more forward-looking perspective in a recent article where we mapped out the 3 likely interest rate trajectories. Here, we provide a more historical perspective on interest rate cycles. We hope this balanced approach will help homeowners grappling with the dilemma of fixed versus floating rate to find an answer.

Rather than the type of interest rate per se, I think it may be appropriate time to refocus on the myriad of home loan features offered by banks these days, which can have more important implications and usefulness to many. In a 3-part series, we will talk about some of these features from the waiver of penalty due to sale, prepayment during lockin period even for fixed rate home loans, to ancillary benefits like earning higher interests on deposit accounts with the same bank. We will cover each one of the 3 local banks, who command more than 80% of the mortgage market in Singapore, to see what are some of the benefits of applying for DBS home loans, OCBC home loans, and UOB home loans. So, watch this space.

Since 2014, MortgageWise.sg has provided thought leadership in the mortgage planning space in Singapore, seeking to build trust with clients over the longer term rather than product-peddling for quick one-time deals. So, be it to refinance home loan, or to buy Singapore condo next, speak to our dedicated team of mortgage consultants here for the best home loan rates.