Should One Stretch Or Shorten His Loan Tenure?

Most are unaware. When one refinances his mortgage, besides the interest rate, one can also review and choose to either increase, decrease or maintain his remaining loan tenure according to his new income situation.

Many would simply focus on getting the best interest rate out there as opposed to what his repricing bank offers. In fact I suspect many other brokers out would just tell their clients to either maintain or stretch his loan tenure for example by another 10 years whenever that is possible subject to TDSR framework and the homeowners’ income-weighted medium age to 75 years old (most banks’ last age to finish servicing a mortgage). Their reasoning – this reduces the monthly instalment and help lesson the burden especially those with more than a few mortgages to service and who also struggle to find tenants in this a challenging market today.

See Top 10 Lowest Home Loan Rates

Certainly that is helpful advice for this group that is somewhat cash-strapped. However, for the majority of homeowners out there who have been prudent with leverage and who service just one mortgage through the years and with his income actually rising during this period, it may make sense to do the reverse, ie. Reduce the loan tenure!

The answer hinges on an understanding of what drives how much interest one actually pays in his monthly mortgage, in other words, how much of the monthly repayment goes to interest and how much goes to principal reduction. Some people may not be aware, besides the nominal interest rate which determines this ratio between interest costs and principal reduction, another variable is the tenure.

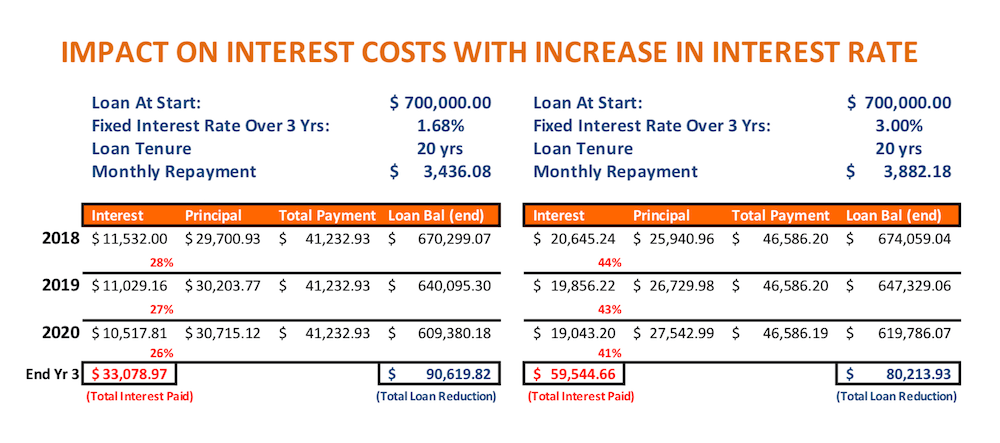

To study the impact on interest component in the monthly mortgage, let us use the case of a typical loan size of $700,000 for private properties on a remaining tenure of 20 years at an interest rate of 1.68%. In the first scenario, we will hold the tenure constant and just show the impact due to rising interest from 1.68% to 3%:

Quite obviously when interest goes up, over a 3-year period, the proportion of interest one pays rises from average of 27% to 43% of the monthly mortgage. And remember the monthly mortgage has also risen by 13% from $3,436 to $3,882. In that sense, it’s like a double whammy where one pays more in monthly repayment and more of it also goes to the bank’s coffers which is the reason why total interest paid over the 3-year period rises by a whopping 80% from $33,078 to $59,544! And the loan reduction is lesser by around $10,000 at the end of three years as more of what one pays go towards interest.

For this reason, those with lock-ins expiring this year should quickly speak to a professional mortgage broker who can still help you lock down fixed rates at below 2% but not for much longer is SIBOR should resume its uptrend. Call us for the best Singapore home loan rates.

In the second scenario, let us hold the interest constant now at 1.68% and vary the tenure instead by extending it 10 more years from 20 years to 30 years:

First observation is that the monthly repayment goes down drastically by almost 30% from $3,436 to $2,476, which is the primary motivation why someone will want to do this. But is the homeowner better off in the long run?

First, we look at what happens over a 3-year period if interest stays constant at 1.68%. The proportion of interest one pays every month goes up from average of 27% to 38%. And because each month more of what one pays goes towards interest, at the end of three years, the amount of loan reduced is a lot lesser than before – only $55,224 versus $90,619 when tenure is 20 years. First implication is that one will take a much longer time to reduce his principal down to zero, and corresponding pays more in interest over the longer 30-year period.

See Top 10 Lowest Home Loan Rates

However, one can also argue that the total interest paid to the bank remains more or less the same at between $33,000 to $34,000 over the 3-year period, so in that sense the homeowner is not paying more interest each year. The only problem is that if one indeed pays down his principal over a much longer 30-year tenure down to the very last year, he would have paid $191,635 in total interests over 30 years as opposed to total interests of $124,658 over 20 years. That is almost $70,000 more or 50% more interest to the bank. And interest does not stay constant at 1.68% over 30 years for sure. When it rises, this figure goes up further.

However, the question to ask is – how many of us would stay in the same house for 30 years, or hold an investment property for 30 years? Not the majority I suspect. Hence if one switches to a longer tenure in a bid to get some reprieve from mortgage obligations every month as a short-term measure, that might still be feasible. Provided there is no intention to serve out the entire stretched tenure and the investor is simply looking to target at a certain holding period before he offloads some units for a profit, and then quickly refinances the remaining mortgages to a shorter tenure, those which he intends to serve out the mortgage.

Whatever the case, homeowers and investors should be made aware that there are actually two drivers – interest rate and tenure, that determines the proportion of interest costs in his or her monthly repayments and do their own calculations to determine what is most optimal for his situation and objective. That would be the purpose of this article.

Since 2014, MortgageWise.sg has provided thought leadership in the mortgage planning space in Singapore, taking deep dives into the latest trends in the industry, providing useful mortgage tips, and making sense of rate movements. We aim to build trust with clients for longer term partnership and not just do product-pushing for a one-time deal unlike bankers. That’s why we always present “whole-of-market” perspective including packages that banks do not pay us. That’s why many have chosen to work with us in the end notwithstanding the sheer number of brokers and agents out there.

{kind=link}

{kind=link}